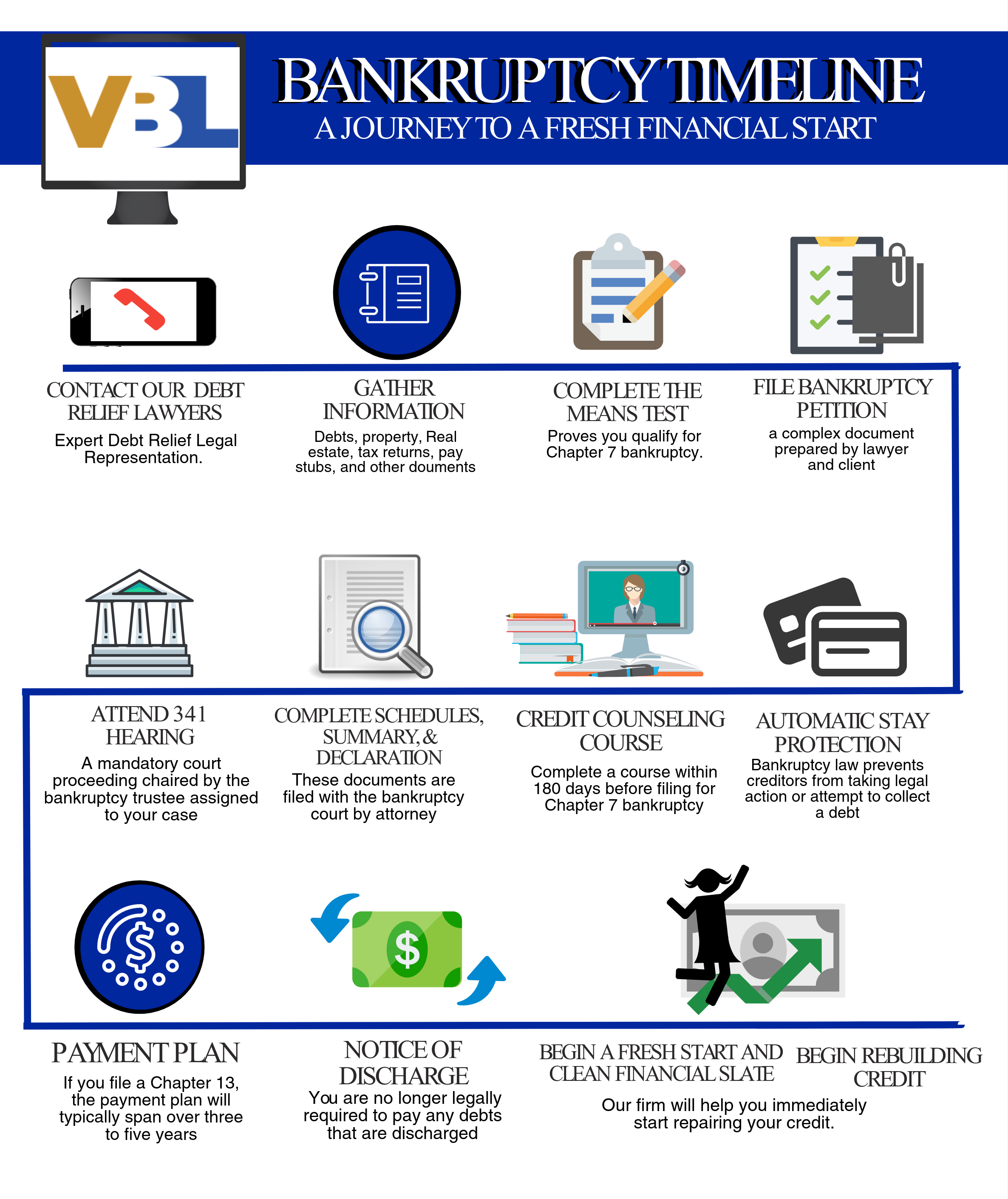

With regards to home loan repayments, prepare yourself making another fee to some other lender. If you are cash-away refis only need you to definitely monthly payment, taking an additional mortgage entails and also make independent monthly installments on the earliest and next bank. This is an issue to trace, thus make sure that you will be making timely costs.

Whenever consumers standard on their financial, 2nd lenders are just settled following original lender is paid back. To help you hedge from this risk, second loan providers demand highest costs. On the confident side, next mortgages feature inexpensive closing costs compared to the bucks-out refis.

When you should Imagine an additional Home loan

Another financial functions if you need to use an enormous count in the place of substitution your existing home loan. Though this one entails investing a higher notice, you reach keep the existing home loan identity and you can rate. 2nd, you should be ready to create a couple of separate mortgage repayments each few days for the rest of the expression. Meanwhile, cash-away refinancing try not to make certain you’ll get the same speed. Unless you’re interested in changing your own price, it does not sound right to take a cash-out refi, especially if you can’t receive a lesser price.

Getting the next home loan allows you to decide how to attract currency. When you find yourself considering delivering money http://www.paydayloancolorado.net/manitou-springs by way of a beneficial revolving line of borrowing, you could potentially prefer a HELOC. Likewise, if you’ve ount, you could potentially withdraw a single-go out lump sum payment having a property guarantee financing. Almost all individuals which have 2nd mortgage loans favor HELOCS, and that account for around ninety% regarding 2nd mortgages.

Household Guarantee Line of credit (HELOC)

HELOCs will be greatest choice if you wish to borrow money as needed. It setting like credit cards, that delivers a great rotating line of credit. That it liberty will make it popular with individuals, letting them safety expanded expenditures. You can withdraw doing a great pre-accepted limit if you find yourself paying interest just towards amount you owe. However, due to the fact a disadvantage, you can even easily be tempted to remain taking money. That said, be careful not to withdraw along side limit.

HELOCs is planned that have a draw several months which usually lasts for the first ten years. Within the mark several months, you can withdraw currency as required into the accepted limitation. While the mark period ends, you are not any longer permitted to grab money. The remaining title try earmarked getting paying back your financial.

HELOCs come that have varying interest rates, which means your monthly obligations vary depending on the latest market conditions. The erratic costs is tough to would. You ought to plan higher monthly obligations when rates of interest rise. On the other hand, you really have lowest monthly premiums if the interest levels to alter all the way down. HELOCs include rates hats to help keep your life speed of broadening way too high. However, if you may be staying an effective HELOC getting fifteen otherwise 2 decades, writing on growing costs is going to be an inconvenience. Be equipped for this downside when taking this.

If you’re HELOCs do not always incorporate closing costs, certain loan providers might need $300 to help you $400 getting domestic appraisals. Loan providers and charges a $100 annual fee to keep your HELOC membership in-service.

House Security Loan

A house guarantee mortgage is provided to help you individuals as a single-go out lump sum matter. It’s an useful solution if you like financing for instant or short-title expenses. Such as, you want $fifty,000 to complete renovations and you may solutions. Which amount is provided with from the lender, then you definitely shell out it when you look at the monthly premiums through your loan’s kept term. Because household collateral loans provide a single-go out dollars-away, you must imagine exactly how much you will want to use. If you want extra money, you can not simply draw currency just as in an effective HELOC. Thus, family collateral financing are not once the popular with consumers.